USSD Financial Services in Africa: Build Mobile Money Experiences

Mobile money transactions in Africa reached $1.105 trillion in 2024 — a 15% increase from 2023 (GSMA State of the Industry Report 2025). USSD powers the majority of them.

If you’re building USSD financial services in Africa, USSD is your primary delivery channel. It works on every phone. It costs customers nothing in data.

And it reaches the 1.1 billion registered mobile money accounts across Sub-Saharan Africa (GSMA 2025).

This guide covers the six financial services you can deliver via USSD, verified case studies from Africa’s biggest mobile money platforms, security best practices, the regulatory landscape, and how to build your own USSD mobile money experience with Arkesel USSD Solutions.

What USSD Means for Financial Services

USSD (Unstructured Supplementary Service Data) is a real-time communication protocol built into every GSM phone. In financial services, it transforms any mobile device into a banking terminal.

A customer dials a shortcode like *170# or *334#. A session opens. They navigate menus to send money, check balances, pay bills, or apply for loans.

No smartphone required. No internet connection. No app download.

This is why USSD captured 63.5% of all mobile money transaction volume in Africa in 2024 (Market Data Forecast). In the West African Economic and Monetary Union (WAEMU) region, that figure reaches 89% (Central Bank of West African States).

For banks, fintechs, and insurance companies operating in Africa, USSD is the channel that reaches your entire addressable market.

Why USSD Dominates Financial Services in Africa

Three factors make USSD the default channel for financial services delivery across the continent.

Universal Device Reach

USSD works on every GSM phone ever made.

Feature phones. Smartphones. First-generation handsets.

In markets where smartphone penetration varies dramatically by region and income level, USSD ensures no customer is excluded from financial services.

Zero Data Cost

USSD sessions don’t consume mobile data. Customers pay nothing to access their accounts, send money, or check balances.

This matters in markets where data costs represent a meaningful share of disposable income.

Real-Time Session Management

USSD sessions are live, interactive connections. The server responds instantly. Customers complete transactions in seconds.

For time-sensitive financial operations — payments, transfers, loan approvals — this speed is essential.

The Numbers Behind the Dominance

Sub-Saharan Africa holds 1.1 billion registered mobile money accounts, representing 53% of the global 2.1 billion total (GSMA 2025).

40% of adults in Sub-Saharan Africa now have a mobile money account — the highest of any world region, up from 27% three years ago (World Bank Global Findex 2025).

Mobile money contributed approximately $190 billion to Sub-Saharan Africa’s GDP in 2023, boosting GDP by more than 5% in about a dozen African countries (GSMA 2025).

The agent network supporting this ecosystem has reached 28 million registered agents globally, with 77% of growth coming from Sub-Saharan Africa (GSMA 2025).

USSD is the primary interface for this entire ecosystem.

6 Financial Services You Can Deliver via USSD

USSD isn’t limited to routine money transfers. As a USSD payment solution in Africa, it powers a full spectrum of financial products across the continent.

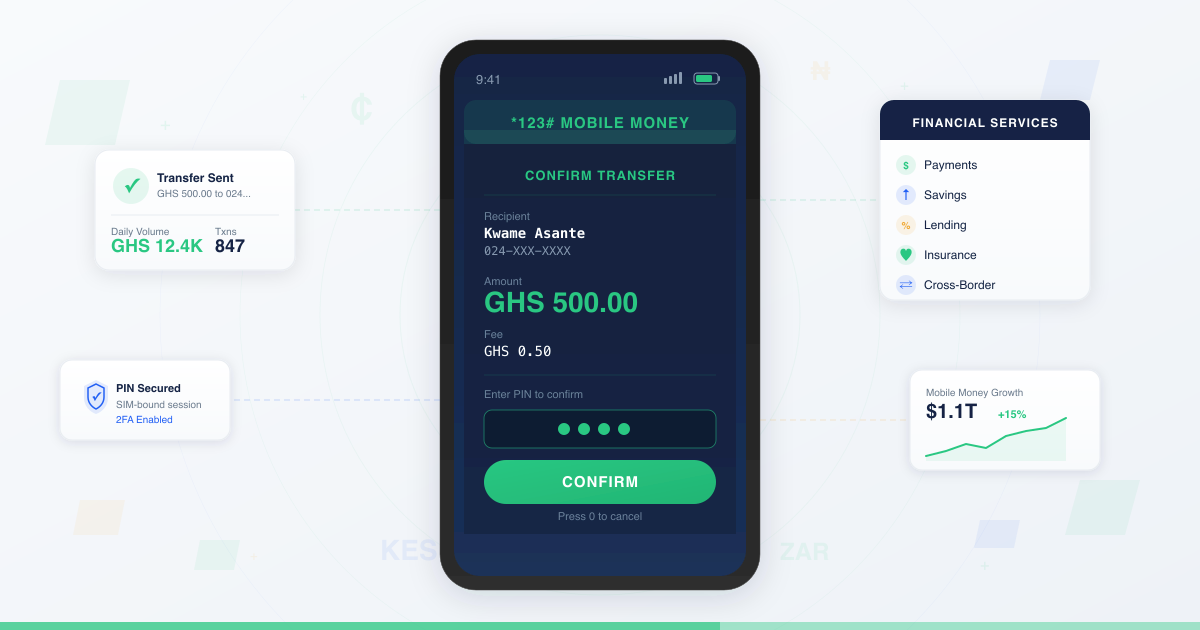

1. Payments and Transfers

The most common USSD financial service. Customers send money to other users, pay merchants, settle bills, and purchase airtime through menu-driven flows.

A typical payment flow:

*123# > Send Money > Enter Number > Enter Amount > Confirm with PIN > DoneFive steps. Under 30 seconds. No data required.

Global mobile money merchant payments reached $105 billion in 2024, with bill payments at $93 billion and bulk disbursements at $97 billion (GSMA SOTIR 2025). USSD handles the lion’s share of these across African markets.

2. Savings and Deposits

USSD makes savings accessible to populations that never had a bank account. Customers open savings wallets, set recurring deposits, and track balances through structured menus.

Microfinance institutions use USSD to offer group savings products. Members deposit weekly, track contributions, and receive automated payout notifications — all without visiting a branch.

3. Lending and Credit

Instant loan disbursement via USSD is one of the fastest-growing USSD fintech services in Africa. Customers apply, get scored, and receive funds in their mobile wallet within minutes.

The flow:

*123# > Loans > Apply > Select Amount > Accept Terms > Funds DepositedNo branch visit. No paperwork. The loan arrives in the customer’s mobile money wallet before they finish their next conversation.

4. Insurance and Microinsurance

USSD unlocks insurance for markets where traditional distribution is impractical. Customers enroll in health, crop, or life insurance through a series of menus, pay premiums via mobile money deduction, and file claims without visiting an office.

Agricultural insurance stands out as a transformative use case. ACRE Africa covers approximately 1.7 million smallholder farmers across East Africa with index-based microinsurance delivered through USSD and mobile money (GSMA Mobile for Development).

Farmers dial a USSD code, select their crop type and coverage level, and pay premiums directly from their mobile wallet. When weather events trigger payouts, funds arrive automatically. The vast majority of smallholder farmers in Africa still lack any insurance coverage — making USSD the most practical distribution channel for closing this gap.

5. Account Management and KYC

Beyond transactions, USSD handles account operations: balance inquiries, mini-statements, PIN changes, and Know Your Customer (KYC) verification for regulatory compliance.

Customers update personal details, set transaction limits, and manage beneficiaries through self-service USSD menus. This reduces the load on call centers and branch staff.

6. Cross-Border Payments and Remittances

Cross-border mobile money is accelerating across Africa. USSD-initiated international transfers let customers send money across borders without visiting an agent or using a smartphone app.

Africa’s instant payment systems processed 64 billion transactions worth nearly $2 trillion in 2024 (AfricaNenda SIIPS 2025). New infrastructure is connecting these systems across borders.

The Pan-African Payment and Settlement System (PAPSS) now connects over 160 commercial banks. A 2026 partnership between Pesalink and PAPSS powers cross-border mobile money payments in local currencies across Kenya’s 80+ bank, fintech, and SACCO network (Afreximbank).

For USSD-first financial services, this means customers can initiate cross-border transfers from any phone, in their local currency, settling instantly on the other end.

See how USSD for business in Africa extends beyond financial services into customer engagement, surveys, and loyalty programs.

How Africa’s Biggest Platforms Use USSD for Mobile Money

These are verified case studies with sourced data from the continent’s leading mobile money platforms.

M-Pesa: The Original USSD Financial Service

M-Pesa, launched by Safaricom in Kenya in 2007, built the entire mobile money industry on USSD. Customers dial *334# to access a full suite of financial services: send money, pay bills, save, borrow, and buy insurance.

The scale: 66.2 million customers across Africa, processing KES 40 trillion ($309 billion) in transactions across 28 billion individual transactions in FY2023/24 (Safaricom).

In Kenya alone, 40 million customers actively use the service. A network of 381,000 agents extends M-Pesa into every corner of the country.

Even with 3.6 million customers on the smartphone app, USSD remains the dominant access point. M-Pesa proves USSD isn’t a stopgap — it’s a permanent financial services delivery channel.

MTN MoMo: Scaling USSD Mobile Money Across 16 Markets

MTN Mobile Money operates across 16 African countries, reaching 64.3 million monthly active users. Fintech transaction value hit $342.3 billion — up 38% year-over-year (MTN Group Q3 2025).

In Ghana, MTN MoMo dominates with 17.7 million active users and 73% market share. MoMo revenue reached GHS 4.3 billion, up 39.2% (MTN Ghana / Mobile Money Africa).

Ghana’s broader mobile money ecosystem tells a powerful story. Transactions reached GHS 3.01 trillion in 2024 — a 56.8% increase from GHS 1.92 trillion in 2023 (Bank of Ghana). Transaction volumes rose 18.9% to 8.1 billion, with average transaction value climbing 32.3% to GHS 372.

The momentum continues: GHS 3.6 trillion in the first 10 months of 2025 alone (Bank of Ghana).

Over 24,000 developers build on MoMo’s open APIs, with 1,600+ live production partners extending the platform’s reach.

Equity Bank *247#: USSD Mobile Banking Pioneer in Africa

Equity Bank launched Africa’s first USSD banking service in 2004 with *247#. Two decades later, it remains one of the most comprehensive USSD mobile banking platforms in Africa.

The *247# service works on all Kenyan networks — Safaricom, Airtel, Telkom, and Equitel — and on any mobile device (Business Daily Africa). Customers access full banking services: transfers, bill payments, balance checks, and mini-statements.

The bank onboarded 60,000+ merchants via its EazzyPay platform and migrated 4 million+ customers to mobile banking in under 20 days (Modefin case study).

Equity Bank demonstrates that USSD banking isn’t just for mobile money operators. Traditional banks can deliver a full banking experience over USSD.

USSD vs App vs Agent: Choosing the Right Financial Services Channel

USSD isn’t the only delivery channel. Here’s how it compares to mobile apps and agent networks for financial services.

| Factor | USSD | Mobile App | Agent Network |

|---|---|---|---|

| Device requirement | Any GSM phone | Smartphone | None (agent’s device) |

| Data requirement | None | Mobile data / WiFi | None |

| Setup for customer | Dial a code | Download, install, register | Visit a physical location |

| Transaction speed | Seconds | Seconds | Minutes (queuing, verification) |

| Service depth | Menu-driven, up to 8 levels | Full UI, unlimited complexity | Agent-assisted, any complexity |

| Security | PIN + SIM-bound session | PIN/biometrics + device-bound | Agent verification + ID |

| Reach | Universal | Smartphone owners only | Limited by agent locations |

| Cost to provider | Low (session-based) | High (development, maintenance) | High (agent commission, training) |

| Best for | High-volume, routine transactions | Complex services, data-rich UX | Cash-in/cash-out, onboarding |

The winning strategy isn’t choosing one channel. It’s layering all three.

USSD handles the volume. The app serves power users. Agents manage cash operations and onboarding.

For a deeper comparison of digital channels, see USSD vs mobile app in Africa and this guide to choosing the right channel mix for African customers.

Securing USSD Financial Transactions

Security is the most overlooked dimension of USSD financial services in Africa. And the gap is significant.

About half of mobile money users in Sub-Saharan Africa do not have a password or PIN protecting their accounts (World Bank Global Findex 2025). For financial services providers, this is both a risk and a design imperative.

PIN Best Practices

Every USSD financial transaction must require PIN authentication at the confirmation step — not at session start. This prevents PIN fatigue (users abandoning sessions because of upfront friction) while securing the moment that matters.

Enforce minimum PIN complexity. Reject sequential patterns (1234) and repeated digits (0000). Prompt users to set a PIN on first use and require periodic changes.

SIM Swap Fraud Protection

SIM swap fraud is the most common attack vector against USSD financial services. An attacker convinces a mobile operator to transfer a victim’s number to a new SIM, then uses USSD to drain the associated mobile money account.

Countermeasures for USSD financial service providers:

- Flag recently swapped SIMs (within 24-72 hours) and require additional verification before high-value transactions

- Implement transaction velocity limits — unusual patterns trigger temporary holds

- Send SMS alerts on every transaction so account holders catch unauthorized activity immediately

Session Security

USSD sessions transmit over GSM signaling channels, which lack end-to-end encryption. The session data passes through the mobile network operator’s infrastructure in cleartext.

For financial services, this means:

- Never display full account numbers in USSD menus — mask all but the last four digits

- Keep sessions as short as possible to minimize the exposure window

- Implement automatic session termination after 60 seconds of inactivity (well below the 180-second network timeout)

Two-Factor for High-Value Transactions

For transactions above a defined threshold, add a second factor. The most practical approach for USSD: complete the transaction flow via USSD, then require confirmation via an SMS code sent to the registered number before final settlement.

This adds seconds, not minutes, to the process — while dramatically reducing fraud exposure on large transfers.

The Regulatory and Interoperability Landscape

The regulatory environment for USSD financial services in Africa is evolving rapidly. Understanding these shifts is essential for any provider building or scaling USSD-based financial products.

Nigeria: USSD Pricing Resolution

Nigeria’s USSD financial services market was constrained for years by a pricing dispute between banks and telecom operators. Banks owed telcos approximately N300 billion in accumulated USSD access fees.

In February 2026, banks and telcos resolved this backlog. The new consumer pricing model sets USSD access at N6.98 per 120-second session (subject to regulatory change) (ALTON / Brand Communicator). This clarity removes a major barrier to USSD financial service investment in Nigeria.

For providers, the fixed-session pricing model makes unit economics predictable. You can now model exactly what each customer transaction costs in USSD access fees.

Ghana: Interoperability Surge

Ghana’s mobile money interoperability infrastructure — which lets customers send money across different mobile money networks seamlessly — is driving explosive growth.

Interoperable transaction value rose from GHS 3.1 billion in December 2024 to GHS 5.8 billion in December 2025, an 87% increase (Bank of Ghana). This means USSD-initiated transfers increasingly cross network boundaries without friction.

Ghana now hosts 74.1 million registered mobile money accounts (Bank of Ghana, February 2025) in a country of approximately 34 million people — reflecting the widespread use of multiple accounts.

Cross-Border Infrastructure: PAPSS

The Pan-African Payment and Settlement System (PAPSS) is building the rails for cross-border USSD financial services. With over 160 connected commercial banks and new partnerships enabling local-currency settlement, PAPSS is removing the friction that previously made cross-border mobile money transfers slow and expensive.

For USSD providers, this infrastructure means you can offer customers cross-border transfer capabilities initiated from a single shortcode dial — settling in the recipient’s local currency on the other end.

How to Design a USSD Mobile Money Experience

Designing USSD menus for financial transactions demands precision. Every extra step risks a dropped session. Every unclear label risks a failed transaction.

For comprehensive guidance on menu structures, see USSD menu design best practices.

Respect Session Time Limits

USSD sessions typically timeout after 180 seconds. Financial transactions must complete well within that window.

Design your flows to reach confirmation in 5 steps or fewer. If a transaction requires more inputs, break it into multiple sessions with saved state.

Design for the Smallest Screen

USSD menus display on screens as small as 160 characters. Keep menu labels short.

Use numbers for navigation. Eliminate decorative text.

Good: 1. Send Money 2. Balance 3. Loans 4. Bills

Bad: Please select from the following options to proceed with your financial transaction today:

Handle Errors Gracefully

Invalid inputs happen constantly. Instead of ending the session, loop back to the last valid step with a clear error message.

Invalid amount. Enter amount (min 1, max 10,000):Never force customers to restart a multi-step transaction because of a single typo.

Build for Multilingual Users

African markets are multilingual. Offer language selection at session start, and maintain that preference across future sessions.

Financial terminology must be tested with native speakers to avoid ambiguity in transaction descriptions and confirmation screens.

How Arkesel Powers USSD Financial Services in Africa

Arkesel’s USSD Solutions are built for Africa’s financial services sector. The platform delivers the capabilities banks, fintechs, and insurance companies need to launch and scale USSD-based products.

Custom USSD Code Provisioning. Get your own dedicated shortcode, provisioned across major networks. Your customers dial your code, access your service.

Ready to get a USSD shortcode for your business in Ghana? Arkesel handles provisioning across all major networks.

Multi-Level Menu API. Build sophisticated financial transaction flows with multi-level menus. Payments, savings, lending, insurance, account management — all structured within a single USSD experience.

Session Management. Real-time session handling ensures transactions complete reliably. Timeout management, state persistence, and error recovery are built into the platform.

Zero Data Cost for Customers. Your customers access financial services without spending a pesewa on data. This removes the biggest adoption barrier in price-sensitive markets.

Enterprise-Grade Reliability. Financial transactions demand 99.9% uptime. Arkesel delivers it, backed by ISO 27001 certification and direct network connections to MTN, Vodafone, and AirtelTigo.

Getting Started: Launch Your USSD Financial Service

Step 1: Define your financial service flows.

Map every transaction your customers need: payments, balance checks, transfers, loan applications, insurance enrollment. Prioritize the three highest-volume transactions for your initial launch.

Step 2: Design your USSD menu structure.

Keep it under 5 levels deep. Place the most-used services at the top of the menu. Test the flow with real users before going live.

Step 3: Address regulatory requirements.

Confirm USSD session pricing in your target market. In Nigeria, budget for N6.98 per 120-second session (subject to regulatory change).

In Ghana, confirm interoperability requirements if your service spans multiple networks. Ensure KYC flows meet central bank requirements.

Step 4: Get your USSD shortcode.

Sign up with Arkesel and provision your dedicated shortcode. Arkesel handles network registration across MTN, Vodafone, and AirtelTigo.

Step 5: Integrate and launch.

Connect your backend systems (core banking, mobile money, CRM) to Arkesel’s USSD platform via REST API. Review the developer API documentation for integration details. Test end-to-end with live transactions, then roll out to customers.

Frequently Asked Questions

What is USSD in mobile money?

USSD (Unstructured Supplementary Service Data) is the communication protocol that powers mobile money services across Africa. When you dial a shortcode like *170# or *334# to send money, check your balance, or pay a bill, you’re using USSD. It works on every phone, requires no internet, and costs the customer nothing in data charges.

How does USSD work for mobile banking in Africa?

A customer dials a bank or fintech’s USSD shortcode. A live session opens on the mobile network, displaying interactive menus on the phone screen.

The customer navigates menus using number inputs to complete banking transactions: transfers, payments, balance inquiries, and loan applications. The session is secured by PIN authentication and bound to the customer’s SIM card.

What financial services can be delivered via USSD?

USSD supports payments and transfers, savings and deposits, lending and credit disbursement, microinsurance enrollment and claims, bill payments, airtime purchases, cross-border remittances, account management, and KYC verification. Any financial service that can be structured as a menu-driven flow can run on USSD.

How do I build a USSD mobile money experience?

Define your transaction flows, design menus that complete in under 5 steps, obtain a USSD shortcode through a platform like Arkesel, integrate your backend via REST API, and launch. Key design principles: respect session timeouts (180 seconds), authenticate at the confirmation step (not session start), and handle input errors without restarting the session.

Is USSD secure for financial transactions?

USSD financial services are secured through PIN authentication and SIM-bound sessions, but they do have security considerations. USSD sessions transmit over GSM signaling channels without end-to-end encryption, and SIM swap fraud is a known attack vector. Best practices include enforcing PIN complexity, flagging recently swapped SIMs, implementing transaction velocity limits, masking account numbers, and adding two-factor confirmation for high-value transactions.

What is the future of USSD payments in Africa?

USSD payments are growing, not shrinking. Ghana’s mobile money transactions surged from GHS 1.92 trillion in 2023 to GHS 3.01 trillion in 2024 — a 56.8% increase.

Cross-border infrastructure like PAPSS is connecting USSD-initiated payments across borders. Interoperability between networks is expanding rapidly.

Even as smartphone adoption grows, USSD remains the highest-reach, lowest-cost channel for financial services across Africa.

Build Your USSD Financial Service with Arkesel

The African mobile money market is valued at USD 951.41 million in 2025, projected to reach USD 4,324 million by 2034 (Market Data Forecast). The opportunity for banks, fintechs, and insurance companies to reach customers through USSD financial services in Africa is massive — and accelerating.

Arkesel gives you the platform to build, launch, and scale USSD financial services across Africa’s major markets.

Custom shortcode provisioning. Multi-level menu API.

Enterprise-grade reliability. Zero data cost for your customers.

Get started with Arkesel today or contact our team to discuss your financial services USSD project.

Related Articles

- How to Get a USSD Shortcode for Your Business in Ghana — Step-by-step guide covering NCA requirements, code types, costs, and provider selection.

- USSD vs Mobile App in Africa: Which Channel Wins? — Data-backed comparison of USSD and mobile apps as customer channels, with a decision framework for African businesses.

- USSD Menu Design: 10 Best Practices for Higher Completion Rates — Actionable guide to designing USSD menus that maximize completion rates, covering character limits, session timeouts, navigation, and multilingual support.

- How to Build a USSD Application: Developer Guide for Africa